production_data <- aus_production %>%

dplyr::select(Quarter, Beer, Gas, Electricity) %>%

drop_na() %>%

mutate(across(c(Beer, Gas, Electricity), log))Activity36

Extending to Multiple Variables with Structural Breaks

Data Prep: Australian Production (Beer, Gas, Electricity)

Activity 1: Detecting Structural Breaks

Structural Break Detection

Using Chow test and CUSUM for regime shifts:

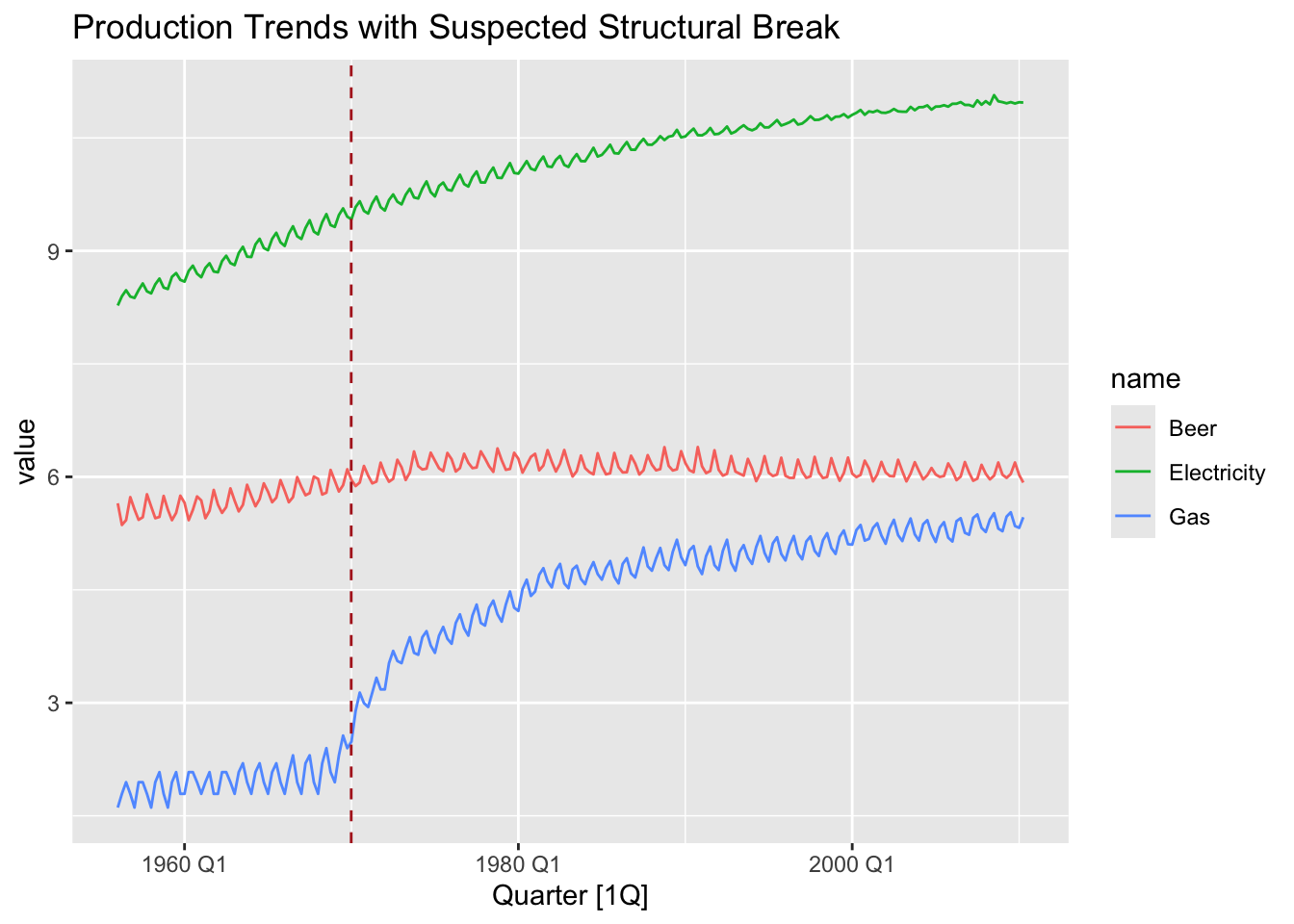

# 1. Visual break identification

production_data %>%

pivot_longer(-Quarter) %>%

autoplot(value) +

geom_vline(

xintercept = as.numeric(yearquarter("1968 Q3")),

color = "firebrick",

linetype = 2

) +

labs(title = "Production Trends with Suspected Structural Break")

# 2. Formal breakpoints test

library(strucchange)

bp_test <- Fstats(Beer ~ Gas + Electricity, data = production_data)

break_date <- breakpoints(bp_test)$breakpoints %>%

production_data$Quarter[.]Handling Structural Breaks

Create intervention dummy:

# Create an intervention dummy: 0 before break, 1 after break

production_data <- production_data %>%

mutate(regime = if_else(Quarter >= break_date, 1, 0))Activity 2: ARIMA with an Intervention Dummy

Incorporating the intervention variable as an external regressor.

# Fit ARIMA model with intervention dummy using xreg()

arima_model <- production_data %>%

model(ARIMA(Beer ~ xreg(regime)))

report(arima_model)Series: Beer

Model: LM w/ ARIMA(3,0,1)(0,1,1)[4] errors

Coefficients:

ar1 ar2 ar3 ma1 sma1 regime

0.4114 0.3476 0.2172 -0.3827 -0.7269 -0.0156

s.e. 0.1396 0.0774 0.1078 0.1339 0.0541 0.0216

sigma^2 estimated as 0.001226: log likelihood=415.13

AIC=-816.25 AICc=-815.71 BIC=-792.69arima_model %>% tidy() %>% filter(term == "regime")# A tibble: 1 × 6

.model term estimate std.error statistic p.value

<chr> <chr> <dbl> <dbl> <dbl> <dbl>

1 ARIMA(Beer ~ xreg(regime)) regime -0.0156 0.0216 -0.724 0.470The underlying model is represented as

\[ \begin{align} y_t &= \mu + \sum_{i=1}^{p}\phi_i y_{t-i} + \sum_{j=1}^{q}\theta_j \epsilon_{t-j} + \beta D_t + \epsilon_t, \end{align} \]

where \(D_t\) is defined as

\[ D_t = \begin{cases} 0, & t < \text{break date}, \\ 1, & t \geq \text{break date}, \end{cases} \]

Activity 3: ETS Models on Regime-Split Data

Since ETS models do not natively accept exogenous regressors, we split the data into pre- and post-break regimes and fit separate ETS models.

# Split the data based on break_date

data_pre_break <- production_data %>% filter(Quarter < break_date)

data_post_break <- production_data %>% filter(Quarter >= break_date)

# Fit ETS models for Beer production on each regime

ets_pre <- data_pre_break %>% model(ETS(Beer))

ets_post <- data_post_break %>% model(ETS(Beer))

# Output summaries

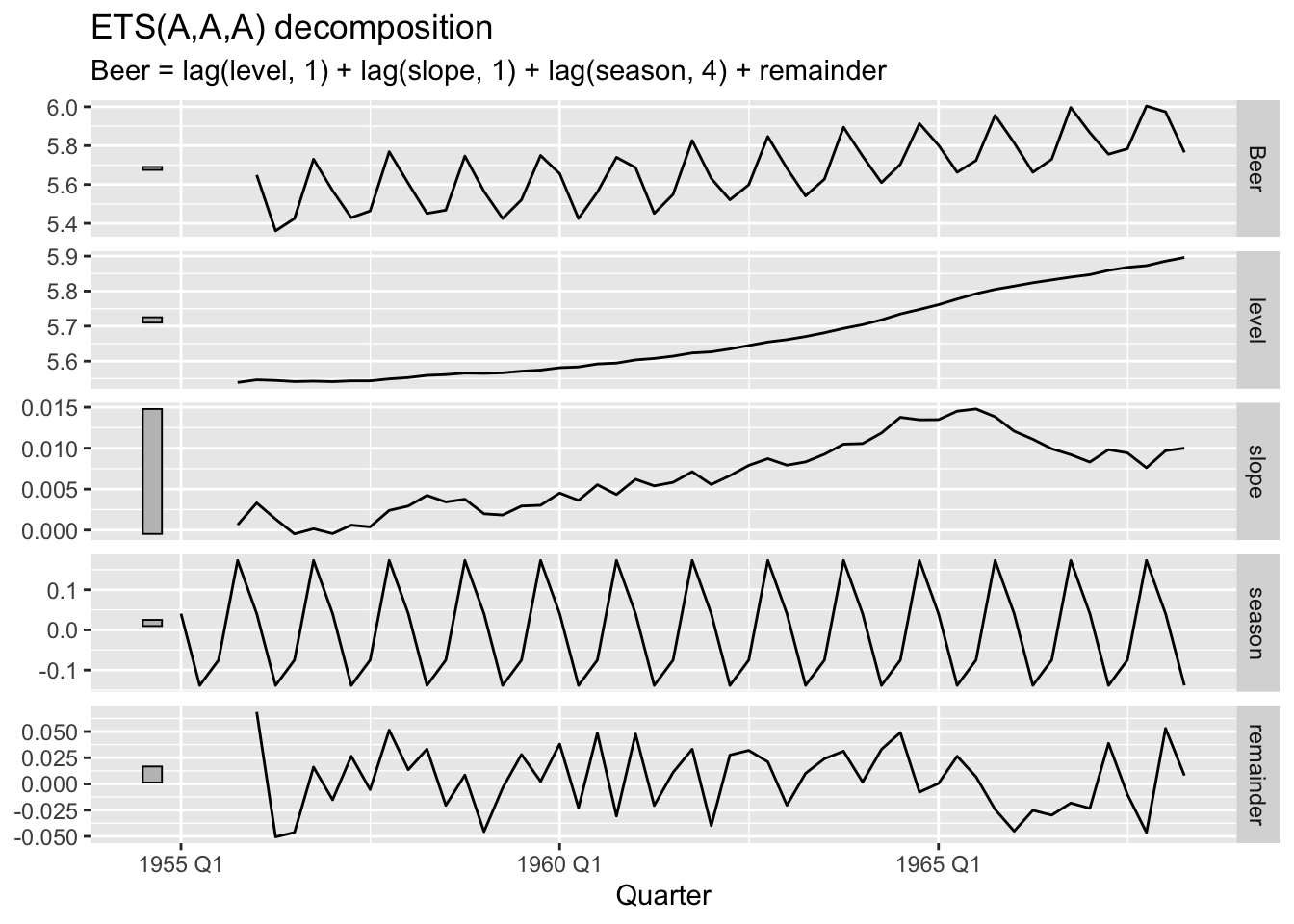

report(ets_pre)Series: Beer

Model: ETS(A,A,A)

Smoothing parameters:

alpha = 0.09973697

beta = 0.03911698

gamma = 0.0001004978

Initial states:

l[0] b[0] s[0] s[-1] s[-2] s[-3]

5.539214 0.0006337494 0.1727994 -0.07509174 -0.1381876 0.04047987

sigma^2: 0.0012

AIC AICc BIC

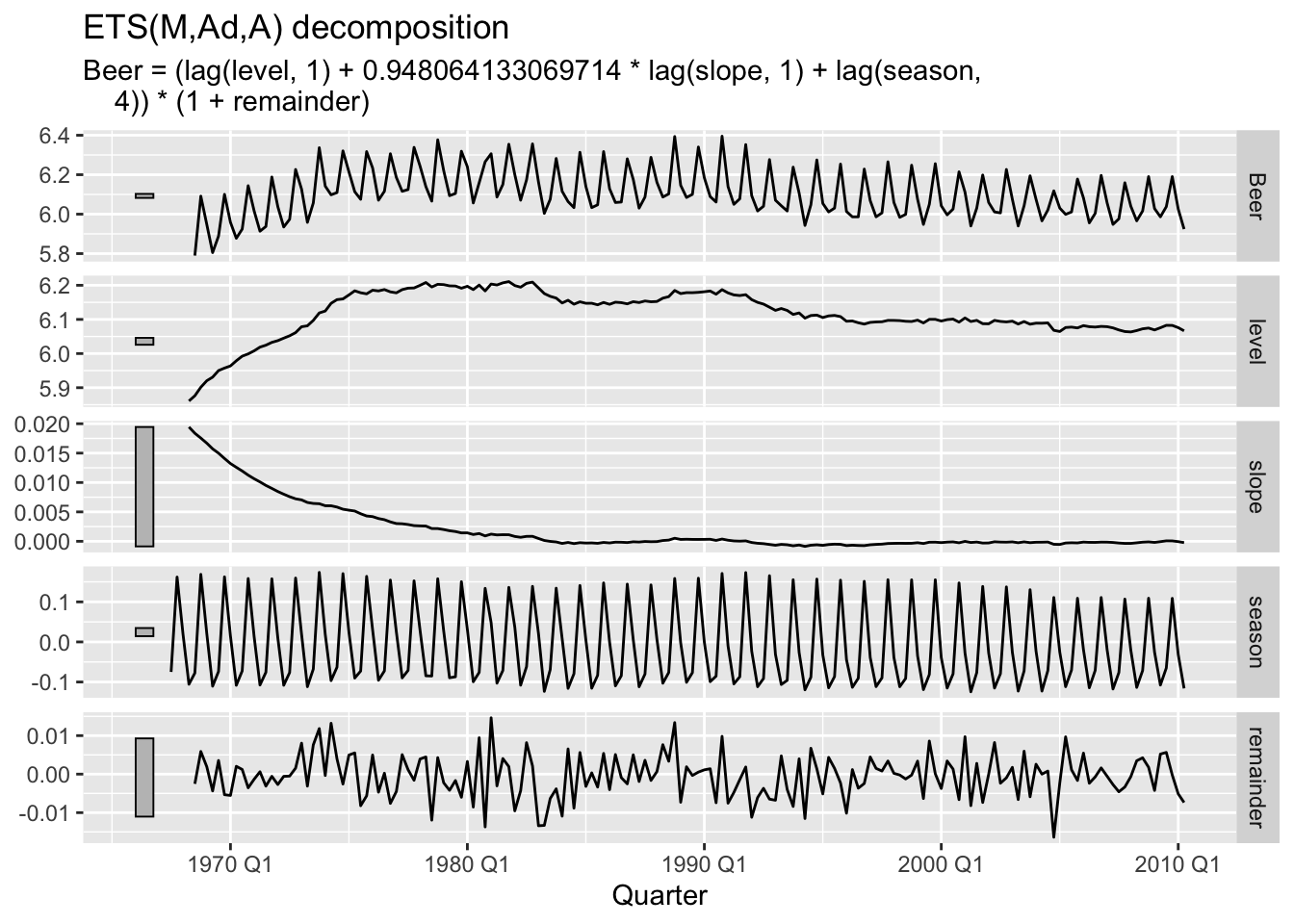

-132.8992 -128.3992 -115.6910 report(ets_post)Series: Beer

Model: ETS(M,Ad,A)

Smoothing parameters:

alpha = 0.2117282

beta = 0.003866127

gamma = 0.1908595

phi = 0.9480641

Initial states:

l[0] b[0] s[0] s[-1] s[-2] s[-3]

5.86103 0.01944297 -0.1056501 0.01861439 0.1619088 -0.07487303

sigma^2: 0

AIC AICc BIC

-249.0023 -247.6010 -217.7627 ets_pre %>%

components() %>%

autoplot()

ets_post %>%

components() %>%

autoplot()