1. SARIMA Model Structure

A SARIMA\((p,d,q)(P,D,Q)_m\) model combines:

- Regular components: AR(p), MA(q) terms for short-term patterns

- Seasonal components: Seasonal AR(P), MA(Q) terms at period \(m\)

- Differencing: \(d\) regular differences + \(D\) seasonal differences

2. Strategic Differencing

Key Principle: Use minimal differencing to stabilize mean/variance

# AirPassengers dataset

ap_ts <- tsibble::as_tsibble(AirPassengers) %>%

index_by(Date = yearmonth(index)) %>%

rename(Passengers = value)

# Automated selection

ap_ts %>%

features(Passengers, list(unitroot_kpss, unitroot_ndiffs, unitroot_nsdiffs))

# A tibble: 1 × 4

kpss_stat kpss_pvalue ndiffs nsdiffs

<dbl> <dbl> <int> <int>

1 2.98 0.01 1 0

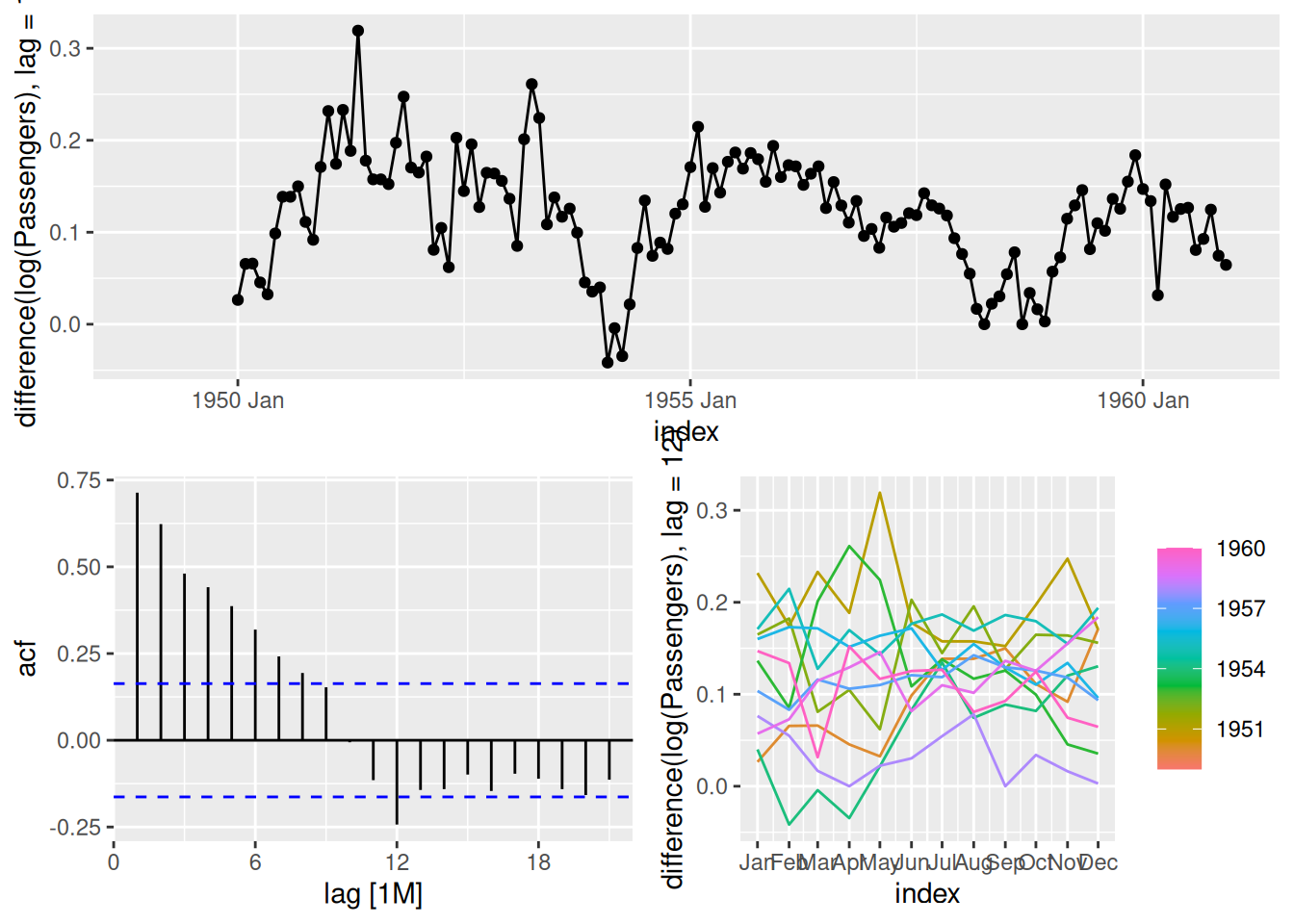

# Visual check

ap_ts %>%

gg_tsdisplay(difference(log(Passengers), lag = 12))

Insight: Seasonal differencing (lag=12) removes yearly patterns while preserving monthly trends

3. Model Building

3.1 Candidate Models

models <- ap_ts %>%

model(

Auto = ARIMA(log(Passengers)),

Manual1 = ARIMA(log(Passengers) ~ pdq(1,1,1) + PDQ(0,1,1, period=12)),

Manual2 = ARIMA(log(Passengers) ~ pdq(2,1,0) + PDQ(1,1,0, period=12))

)

glance(models) %>% arrange(AICc)

# A tibble: 3 × 8

.model sigma2 log_lik AIC AICc BIC ar_roots ma_roots

<chr> <dbl> <dbl> <dbl> <dbl> <dbl> <list> <list>

1 Auto 0.00132 250. -489. -489. -475. <cpl [2]> <cpl [12]>

2 Manual1 0.00137 245. -482. -482. -470. <cpl [1]> <cpl [13]>

3 Manual2 0.00148 241. -474. -473. -462. <cpl [14]> <cpl [0]>

3.2 Coefficient Check

For top model:

final_model <- models %>%

select(Auto)

tidy(models) %>%

filter(.model == "Auto")

# A tibble: 4 × 6

.model term estimate std.error statistic p.value

<chr> <chr> <dbl> <dbl> <dbl> <dbl>

1 Auto ar1 0.575 0.0843 6.83 2.83e-10

2 Auto ar2 0.261 0.0842 3.11 2.33e- 3

3 Auto sma1 -0.555 0.0771 -7.21 3.99e-11

4 Auto constant 0.0193 0.00149 13.0 2.07e-25

4. Model Refinement Cycle

- Start with automatic differencing

- Compare multiple model specifications

- Validate residuals systematically

- Iterate using PACF patterns

# Final refinement example

ap_ts %>%

model(

Best = ARIMA(log(Passengers) ~ pdq(1,1,1) + PDQ(0,1,1, period=12))

) %>%

report()

Series: Passengers

Model: ARIMA(1,1,1)(0,1,1)[12]

Transformation: log(Passengers)

Coefficients:

ar1 ma1 sma1

0.1960 -0.5784 -0.5643

s.e. 0.2475 0.2132 0.0747

sigma^2 estimated as 0.001375: log likelihood=244.95

AIC=-481.9 AICc=-481.58 BIC=-470.4

1. Data Preparation

Q1: Examine the seasonal patterns using gg_season(). What type of seasonality dominates this series?

2. Model Specification

Fit SARIMA(1,1,1)(0,1,1)₁₂ model with maximum likelihood estimation

Q2: Interpret the model structure:

What does the (1,1,1) non-seasonal component represent?

Why do we use PDQ(0,1,1) for seasonal terms?

3. Parameter Estimation

Task: Extract and interpret coefficients

Q3: Which coefficients are statistically significant (α=0.05)? What does the MA(1) coefficient suggest?

4. Residual Diagnostics

4.1 Visual Analysis

Q4: Do residuals show concerning autocorrelation patterns? Justify your answer.

5. Model Validation

Task: Check specification robustness

Q6: Compare AICc values across estimation methods. Does our original model remain preferred?